{kind=link}

It can be tricky to put a price tag on biotechnology companies that offer little more than the promise of success in the future. Just because someone in the lab cries “Eureka!” that doesn’t necessarily mean that a cure has been found. In the biotech sector, it can take many years to determine whether all the effort will translate into returns for a company. However, while valuation may appear to be more guesswork than science, there is a generally accepted approach to valuing biotech companies that are years away from payoff. In this article, we explain this valuation approach, which relies on discounted cash flow (DCF) analysis, and take you through the process step by step.

Portfolio Valuation Approach

Think of a biotech company as a collection of one or more experimental drugs, each representing a potential market opportunity. The idea is to treat each promising drug as a mini-company within a portfolio. Using DCF analysis, you can determine what someone would be willing to pay for that drug portfolio.

In other words, you determine the forecasted free cash flow of each drug to establish its separate present value. Then, you add together the net present value of each drug, along with any cash in the bank, and come up with a fair value for what the whole company is worth today.

A biotech company can have dozens or even hundreds of drugs in its developmental pipeline. However, that does not mean you should include them all in your valuation. Generally speaking, you should only include those drugs that are already in one of the three clinical trial stages. (For more information, visit the U.S. Food and Drug Administration’s website.) As an investment, a drug that is in the discovery or pre-clinical stage is a very risky proposition, with less than a 1% chance of getting to market (according to an industry report published in 2003 by the Pharmaceutical Research and Manufacturers of America). Therefore, drugs in the pre-clinical stage are usually assigned zero value by public market investors.

Forecasting Sales Revenue

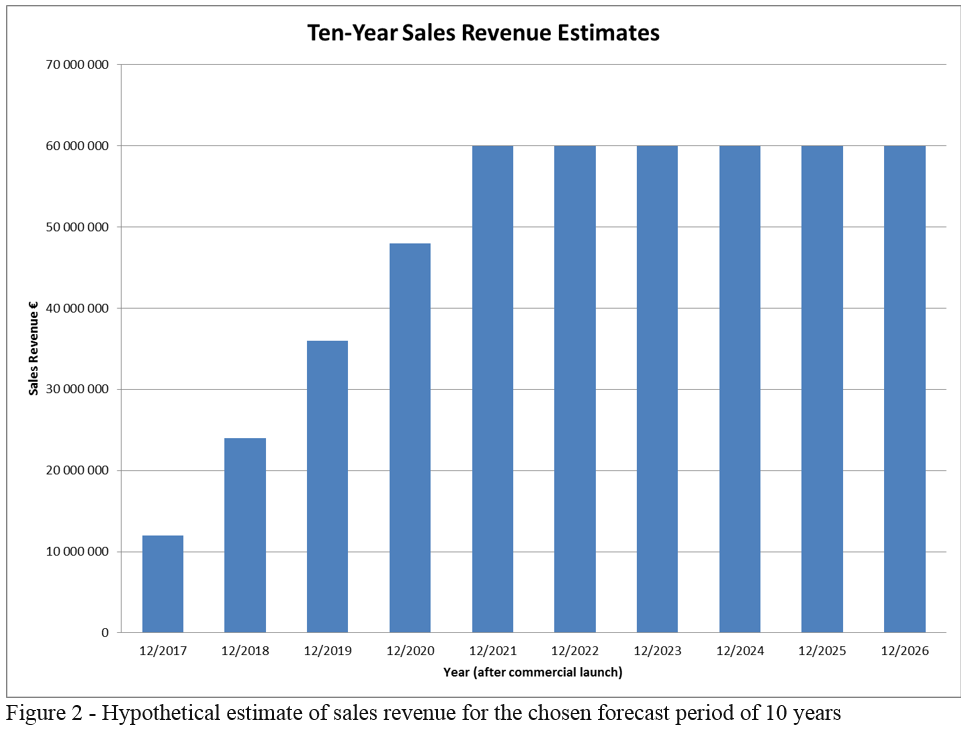

Forecasting the sales revenue from each of a biotech company’s drugs is probably the most important estimate you can make about future cash flows, but it can also be the most difficult. The key is to determine what expected peak sales would be if – and this is a big “if” – a drug successfully makes it all the way through clinical trials. Normally, you will forecast sales for the first 10 years of the drug’s life.

SEE: Great Expectations: Forecasting Sales Growth

Market Potential

You need to start by making assumptions about the drug’s market potential. Look at information provided by the company and market research reports to determine the size of the patient group that will use the drug. Analysts typically focus on market potential in the industrialized countries, where people will pay the market price for drugs.

When making assumptions about a drug’s potential market penetration, you have to use your own best judgment. If there is a competitive drug market, with limited advantage offered by the new drug in terms of increased effectiveness or reduced side effects, the drug will probably not win substantial market share in its product category. You may assume that it will capture 10% of that total market, or even less. On the other hand, if no other drug addresses the same needs, you might assume the drug will enjoy market penetration of 50% or more.

Estimated Price Tag

Once you have established a sales market size, you need to come up with an estimated sales price. Of course, putting a price tag on a drug that addresses an unmet need will involve some guesswork. But for a drug that will compete with existing products, you should look at the price of the competition. For instance, pharmaceutical giant Roche’s recently introduced HIV-inhibitor drug, Fuzeon, costs just over $20,000 per year. Multiplying that price by the estimated number of patients gives you estimated annual peak sales.

The biotech company won’t necessarily receive all of this sales revenue. Many biotech firms – especially the smaller ones with little capital – do not have sales and marketing divisions capable of selling high volumes of drugs. They often license promising drugs to bigger pharmaceutical companies, which help pay for development and become responsible for making sales. In return, the biotech firm normally receives royalty on future sales. According to an article written by Medius Associates (“Royalty Rates: Current Issues and Trends,” October 2001), the royalty rate for drugs currently in Phase I of clinical trials is normally a percentage in the single digits. As these firms move along the development pipeline, royalty rates get higher.

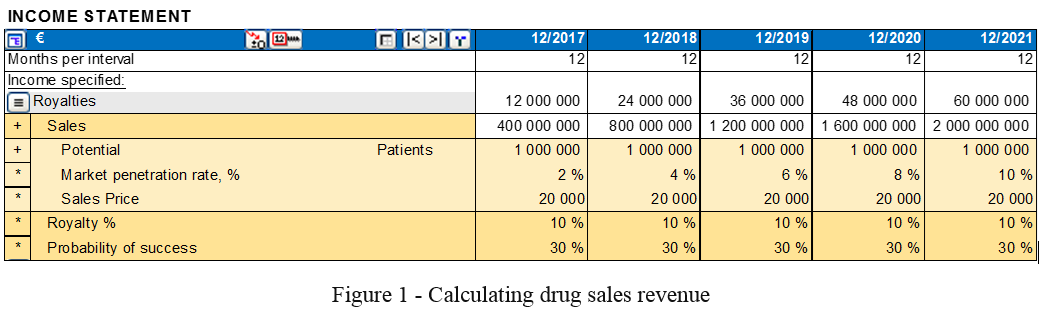

In Figure 1, we break down an estimate of the peak annual sales revenues for a hypothetical biotech drug in a competitive market with a potential market size of 1 million patients, an estimated sales price of $20,000 per year and a royalty rate of 10%.

Drug patents usually last about 10 years. In our hypothetical example, we assume that for the first five years after commercial launch, sales revenues from the drug will increase until they hit their peak. Thereafter, peak sales continue for the remaining life of the patent.

Estimating Costs

When forecasting future cash flows for a drug, you need to consider the costs of discovery and bringing the drug to market.

For starters, there are operating costs associated with the discovery phase, including efforts to discover the drug’s molecular basis, followed by lab and animal tests. Then there is the cost of running clinical trials. This includes the cost of manufacturing the drug, recruiting, treating and caring for the participants, and other administrative expenses. Expenses increase in each development phase. All the while, there is ongoing capital investment in items such as laboratory equipment and facilities.

Taxation and working capital costs also need to be factored in. Investors should expect operating and capital costs to represent no less than 30% of the drug’s royalty-based sales.

By deducting the drug’s operating costs, taxes, net investment and working capital requirements from its sales revenues, you arrive at the amount of free cash flow generated by the drug if it becomes commercial.

Accounting for Risk

Our free cash flow forecast assumes that the drug makes it all the way through clinical trials and is approved by regulators. But we know this doesn’t always happen. So, depending on the drug’s stage of development, we must apply a probability factor to account for its probability of success.

As the drug moves through the development process, the risk decreases with each major milestone. The Pharmaceutical Research and Manufacturers of America reported in 2003 that drugs entering Phase I clinical trials have a 15% probability of becoming a marketable product. For those in Phase II, the odds of success rise to 30%, and for Phase III, they climb to 60%. Once clinical trials are complete and the drug enters the final FDA approval phase, it has a 90% chance of success. These improvements in the odds of success translate directly into stock value.

By multiplying the drug’s estimated free cash flow by the stage-appropriate probability of success, you get a forecast of free cash flows that accounts for development risk.

The next step is to discount the drug’s expected 10-year free cash flows to determine what they are worth today. Because you have already factored in risk by applying the clinical trial probability of success, you do not need to include development risk in the discount rate. You can rely on normal means of calculating the discount rate, such as the weighted average cost of capital (WACC) approach, to come up with the drug’s final discounted cash flow valuation.

What’s the Firm Worth?

Finally, you want to calculate the total value of the biotech firm. Once you have gone through all the steps outlined above to calculate the discounted cash flow for each of the biotech firm’s drugs, you simply need to add them all up to get a total value for the firm’s drug portfolio.

| DCF Value Drug A + DCF Value Drug B + DCF Drug C … … = Total Firm Value |

The Bottom Line

As you can see, valuing early-stage biotech companies is not entirely a black art. Intelligent investors can come up with solid stock valuation estimates if they are familiar with DCF analysis and are equipped with a basic understanding of the industry and how major developmental milestones can impact the value of a biotech firm.

Source: Based on an article by Ben McClure on July 22, 2012 in Investopedia